When the flywheel stops spinning, hardware and software begin to compete for players’ wallets together.

As a gamer, have you noticed that playing games has become more and more expensive?

Everything is Getting More Expensive

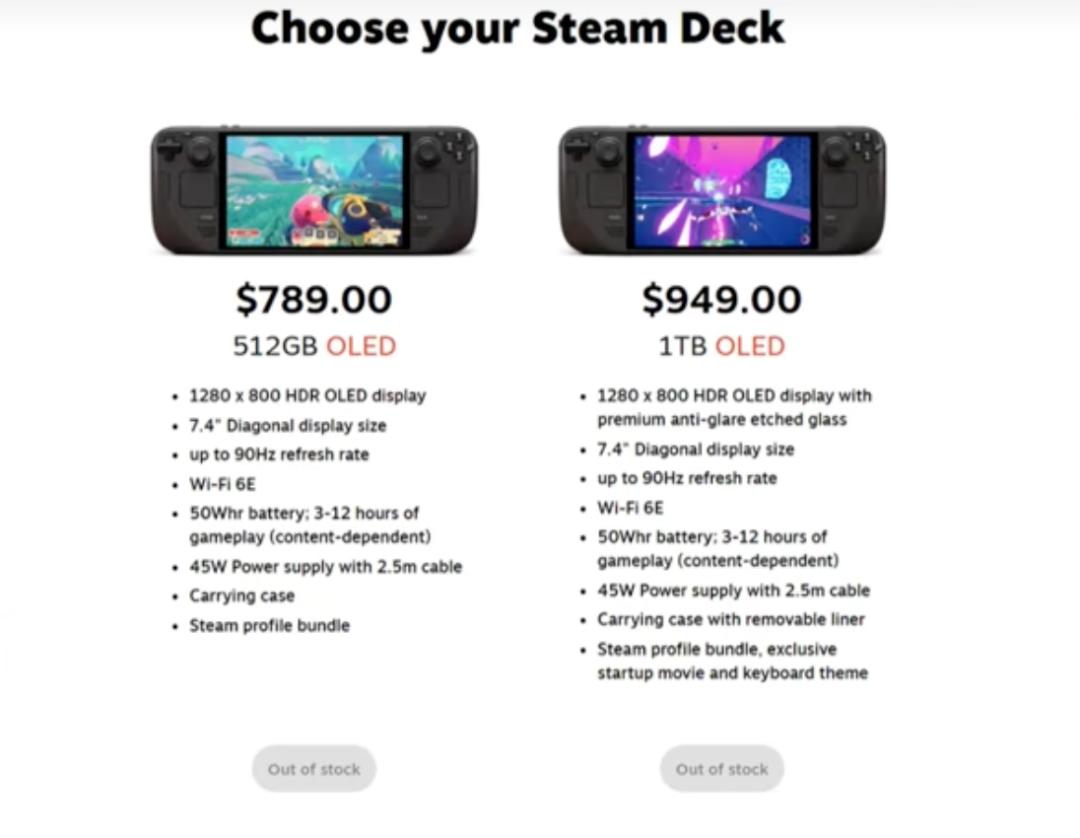

On May 28th this year, Valve announced a price increase for the Steam Deck. The price of the highest – spec 1TB OLED version reached $949 after the increase, with a nearly 50% rise. You know, although the OLED version is relatively new, it’s already a device that has been on the market for nearly 3 years. Moreover, the performance of the OLED version is basically the same as that of the regular Steam Deck launched in 2022

Valve explained that the price increase was due to the rising costs of components and global logistics. However, this is exactly the change that has made players the most uncomfortable in the past two years

This is not an isolated incident. Twenty days before the Steam Deck price increase (on May 8th), Nintendo issued a price – adjustment notice, announcing a simultaneous price increase for the Switch 2 and NSO (Nintendo Switch Online) membership. The price of the Switch 2 in Japan increased by 10,000 yen, and in the United States, it rose from $449 to $499. The prices of different tiers of NSO membership in the Japanese service also increased by about 25%

If we look back a bit further, the launch – accompanying game of the Switch 2, “Mario Kart: World”, raised the software price to $80 last year. In March this year, Nintendo of America announced on its official website that starting from May, the digital – only Nintendo games exclusive to the Switch 2 would have different retail prices from the physical versions. Take “Yoshi and the Unbelievable Picture Book” as an example. The digital version maintained a price of $59, while the physical version became $70.

In the past 30 years, there has been a stable rule in the gaming industry: whether it’s game consoles or PCs, they should become cheaper after being on the market. A new device is expensive at launch because of the new CPU, new architecture, and the fact that the production capacity of the new production line hasn’t been fully ramped up. Meanwhile, at the time of launch, there are always some core players willing to pay a premium to buy it

But under normal circumstances, the price will drop after a few years. More mature components and supply chains, more rational players, and the second – hand market transactions will all drive manufacturers to offer discounts or lower the retail price

This is what we often call “buy early, enjoy early; buy late, get a discount”

In this way, more players can afford the hardware, the installed – base will continue to expand, and software, DLCs, and subscription services will have a larger market to sell to. This is also the most important flywheel for the coordinated growth of hardware and software in the gaming industry in the past 30 years

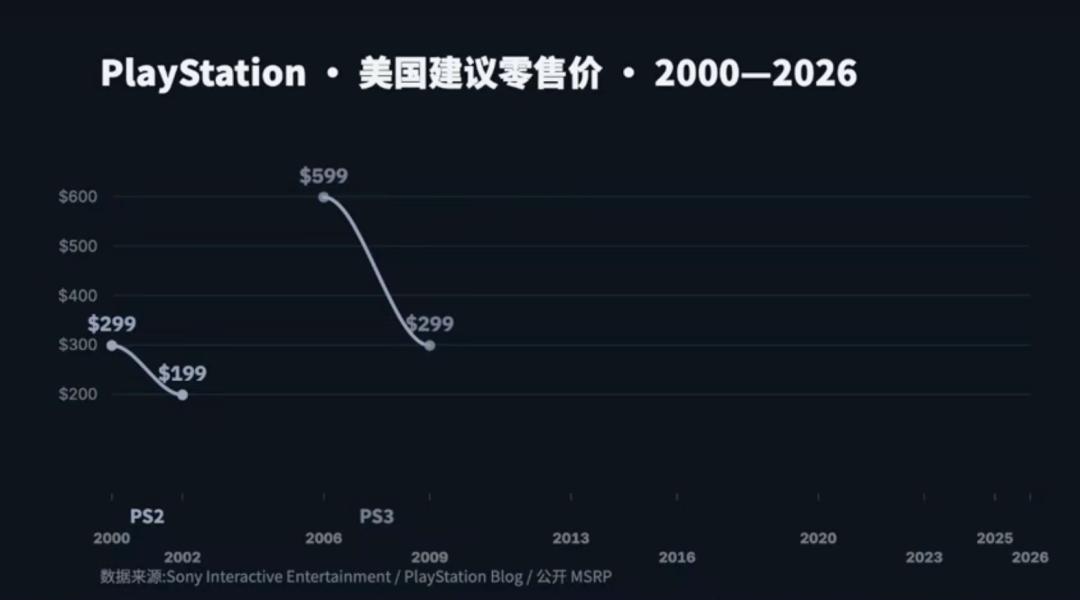

Take the PS2 as an example. When it was launched in North America in 2000, the suggested retail price was $299. By 2002, Sony had reduced the price of the PS2 in the United States to $199

The PS3 is even more typical. It was launched in North America in 2006. The 20GB version was priced at $499, and the 60GB version at $599. In 2009, the new PS3 Slim was launched, and the price dropped to $299. Comparing the most – watched 60GB version at that time, the price of the PS3 was almost halved after three years

Although the price reduction of the PS4 was not as dramatic as that of the PS2 and PS3, the trend was the same. In 2013, when the PS4 was launched in the United States, the price was $399. In 2016, Sony lowered the price of the PS4 Slim to $299

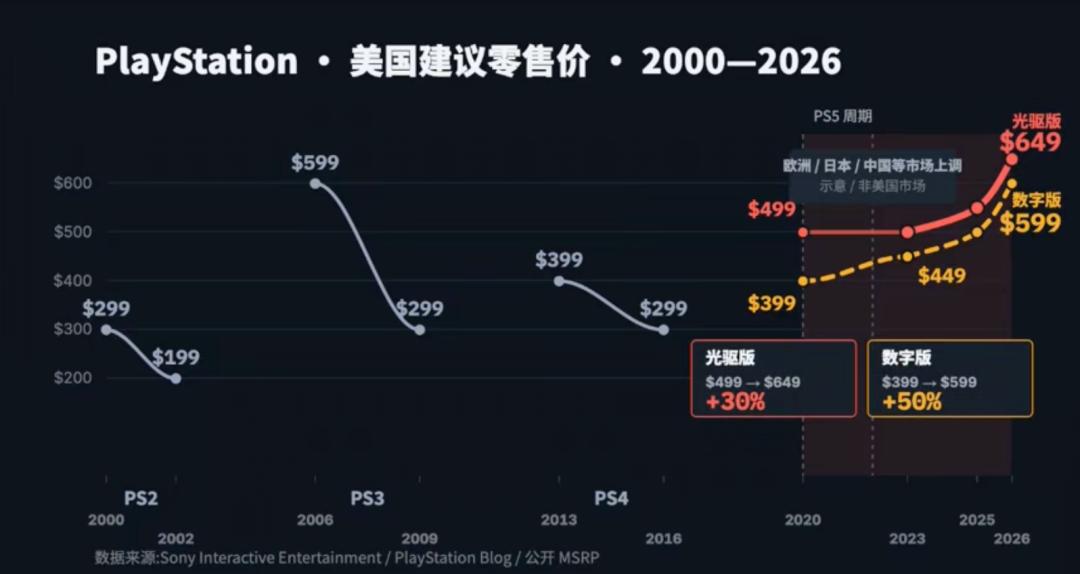

But with the PS5 generation, the curve started to reverse

In 2020, when the PS5 was launched in the United States, the digital version was priced at $399, and the disc – drive version at $499. Three years later, a new miniaturized version of the PS5 was released, but Sony didn’t lower the price. The disc – drive version remained at $499, and the digital version even increased from the initial $399 to $449

After that, Sony started a series of price increases

In 2022, Sony first raised the suggested retail price of the PS5 in markets such as Europe, Japan, and China, citing global inflation and exchange – rate pressure as reasons

In 2025, the price of the PS5 also started to increase in the US market. The disc – drive version rose from $499 to $549, and the digital version to $499. In April this year, Sony announced another global price adjustment. The disc – drive version of the PS5 increased to $649, and the digital version to $599

If we only look at the US market, the price of the PS5 disc – drive version has increased by about 30% from the initial $499 to the current $649. The price of the PS5 digital version has increased by nearly 50% from the initial $399 to the current $599

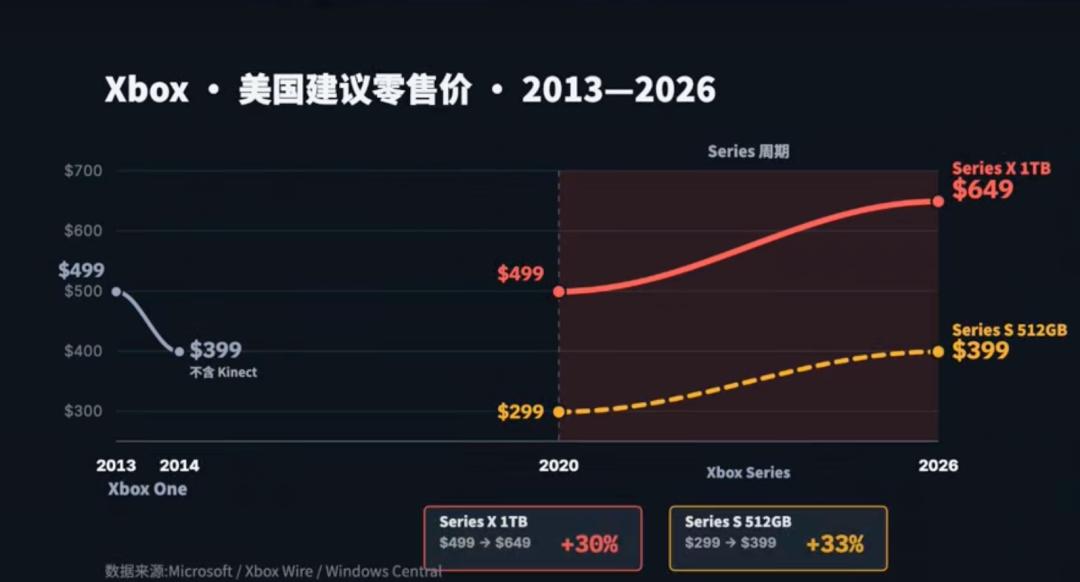

The Xbox is no exception

In 2013, when the Xbox One was launched, the price was $499. Less than a year later, Microsoft launched a version without Kinect and lowered the entry – level price to $399. The Xbox Series X was priced at $499 when launched in 2020, and the Series S at $299. Now, on the official Microsoft website, the price of the 1TB Xbox Series X is $649, and the 512GB Xbox Series S is $399

The Steam Deck has increased in price, the Switch 2 has increased, the PS5 has increased, and the Xbox has increased. On the PC side, needless to say, after the price of graphics cards increased, the price of memory increased, and after the price of memory increased, the price of hard drives increased. The past experience has completely failed. Now, buying early not only allows you to enjoy early but also get a discount

After 2020, PC hardware and the ninth – generation consoles have not followed the previous rule of price reduction

You know, hardware price reduction is not only a benefit for players but also an integral part of the platform expansion strategy

Hardware is the “ticket” that players need to pay before entering the ecosystem. However, this “up – front tax” has not been diluted as the number of payers increases. Instead, it has become higher and higher. This cost no longer guarantees stronger performance. In fact, the price increases of the Steam Deck, PS5, and Switch 2 are all players paying for the profit pressure of manufacturers

Why do console and hardware manufacturers suddenly lose the ability or motivation to make hardware cheaper? The direct reason comes from the upstream

02

There’s No Room for Gamers at the Semiconductor Table

In the past, gamers were the most important group in the supply chain of high – performance consumer electronics

Gamers wanted better graphics, so they needed to buy more powerful graphics cards. The more graphics cards were sold, the more motivated GPU manufacturers were to invest in the next – generation architecture. There used to be a clear common interest between games and semiconductors. Games created demand, and semiconductors raised the technological ceiling

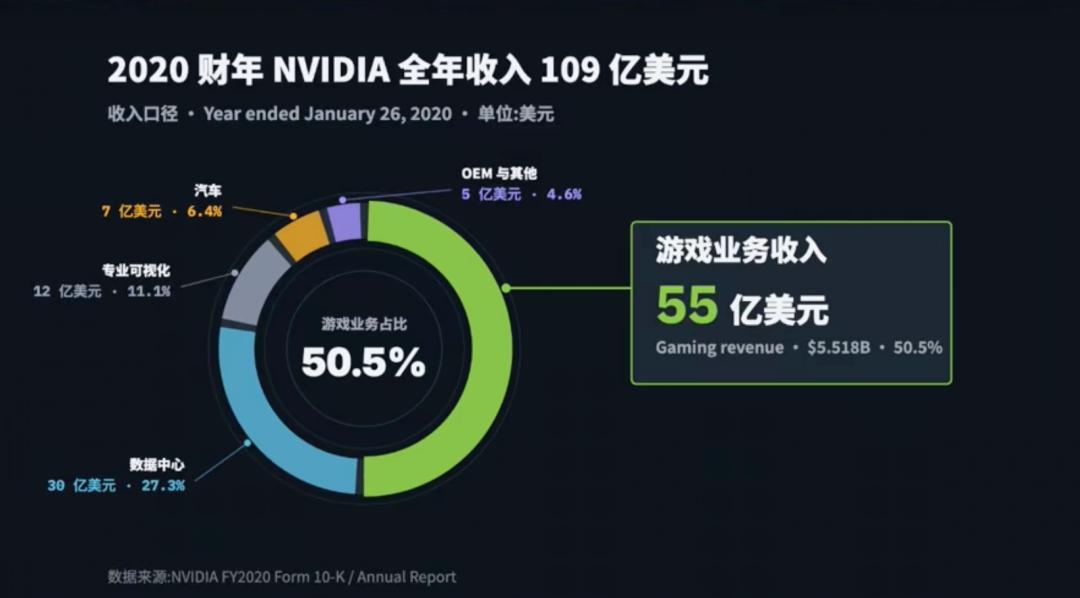

So for a long time in the past, games were the most important customers for Nvidia and AMD. Nvidia’s financial reports also confirm this. In the fiscal year 2020, Nvidia’s annual revenue was $10.9 billion, of which the revenue from game – related businesses was $5.5 billion, accounting for more than half of the company’s total revenue. At that time, games were the most important narrative center for Nvidia

But now, it can almost be said that there’s no room for games at the semiconductor table

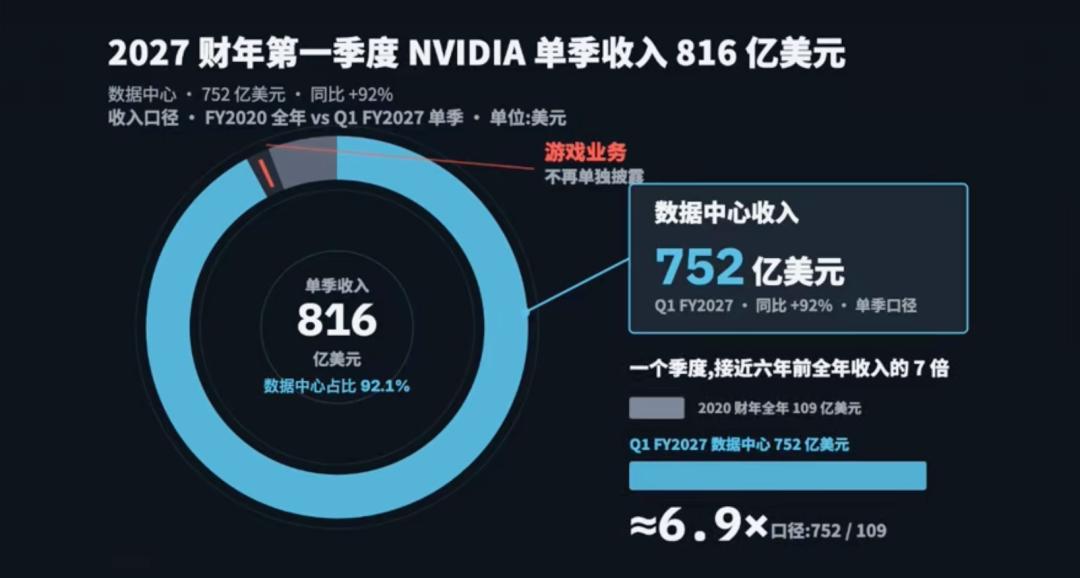

Nvidia’s financial report for the first quarter of the fiscal year 2027 shows that the company’s single – quarter revenue reached $81.6 billion, of which the revenue from the data center was $75.2 billion, a year – on – year increase of 92%. In the most recent quarter, the revenue of the data center in one quarter was nearly seven times that of Nvidia’s annual revenue six years ago

In the latest financial report, games have been included in a new disclosure framework and are no longer disclosed as a separate business. Game – related hardware, workstations, robotics, and autonomous driving and other businesses have been grouped by Nvidia into the Edge Computing business

Games no longer have a central position in Nvidia’s narrative. Graphics cards are still profitable, but gamers are no longer the most important marginal buyers in the high – performance semiconductor supply chain. Now, semiconductor companies give priority to orders from ultra – large – scale data centers and large – model companies

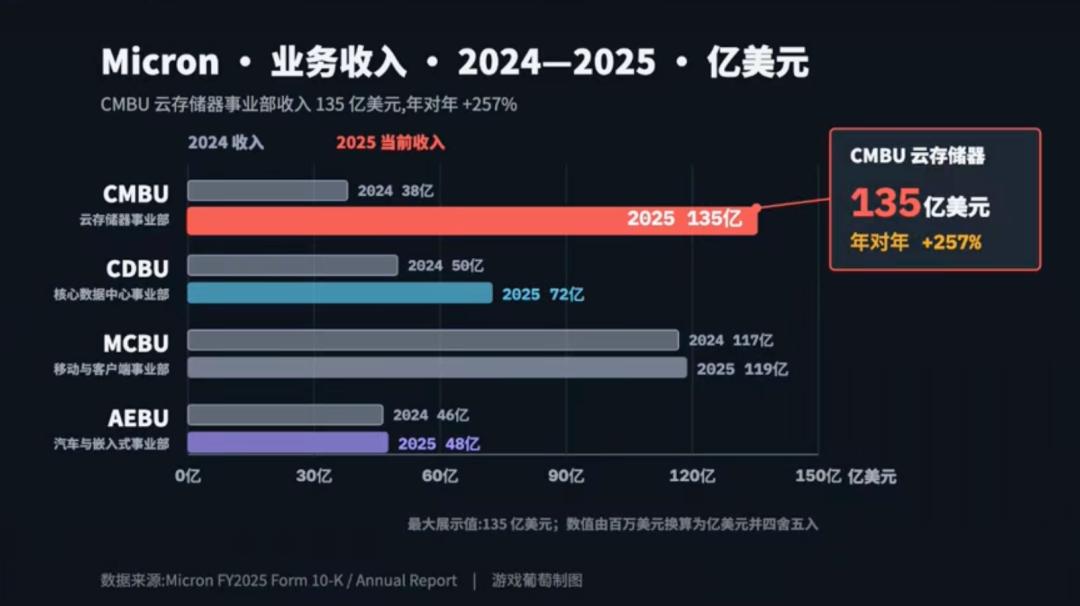

Memory is the best example

In 2025, the revenue of Micron’s cloud memory division was $13.5 billion, a year – on – year increase of 257%. Micron said in its financial report that the company had shifted its memory production capacity to the higher – value data – center market

Even due to the surge in demand for memory and storage caused by AI data centers, in December 2025, Micron directly announced its withdrawal from the Crucial consumer business to improve the supply and support for larger customers. And the large customers they mentioned are those AI companies

The emergence of AI has changed the business logic of game hardware because now time is no longer on the side of gamers

AI data centers bring larger orders and longer procurement cycles to Nvidia and Micron. As a result, we gamers who are still waiting to buy at a discount see that the latest chip production capacity has been pre – locked by large – model companies. In the supply – chain expansion driven by AI companies, the production capacity and priority may not flow back to gamers

This is also the real reason why the game – hardware flywheel has stopped. Gamers may have waited for three years, but instead of waiting for the console price to drop, they have witnessed a price increase after manufacturers recalculate the cost

Because the hardware industry is no longer expanding around games and gamers

03

The War for Gamers’ Wallets

However, I don’t mean that the gaming industry is going to collapse

According to the statistics of ESA, Circana, and Sensor Tower, the total consumption in the US video – game market in 2025 reached $60.7 billion, a 1.4% increase compared to 2024

This was the second – best year in the history of the US game market, second only to the $61.7 billion during the pandemic in 2021